The May 31 inventory in Department B (June’s beginning work in process) consists of 2,000 units that are fully complete as to materials and 60% complete as to conversion. The objective of using equivalent units is to be able to apportion the costs of production to completed units and partially completed units held in work in process. Even though the firm needs an aggregate number to get overall ending WIP value, the firm will want to keep data on how much of that $20,493.81 is due to conversion costs, direct materials, and transferred-in costs.

5.2 FIFO Cost Allocation (STEP #

Therefore, proper costing methodology for 100 units in process would entail 80 equivalent units of material, and 60 equivalent units of conversion (i.e., labor and overhead). If an alternative weighted average method is used then the beginning WIP units are treated dependent motions as started and completed (100%) during the accounting period. The treatment using this method is discussed in our equivalent units of production- weighted average method tutorial. The actual manufacturing process used in process costing firms usually isn’t uniform.

Looking To Get Started?

The overall objective of process costing is to take these costs and redistribute them between (1) ending WIP and (2) the credit side of the WIP account (i.e. completed and transferred out costs). You probably do some consulting (i.e. labor and overhead) with the customer before sending the job to the printer. Notice that direct materials (i.e. the paper and ink) are not applied until toward the end of the process.

4 Weighted Average Rates and Cost Allocation (STEP #2 and STEP #

Unlike the weighted average method, the FIFO method does not involve any averaging out of the total costs incurred during a period. Equivalent units must be considered relative to each of the factors of production. In other words, 80% of necessary direct material may be in process but only 60% of the direct labor and factory overhead.

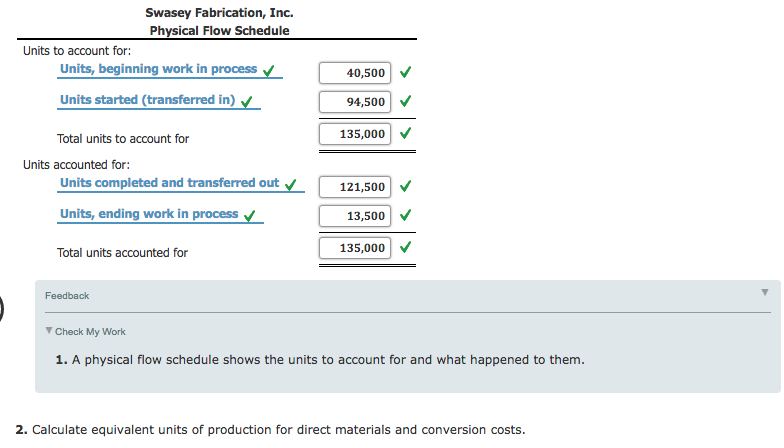

1 Complications with Process Costing

- We already covered how the weighted average and FIFO methods define the denominators differently.

- (1) Get a pot of water out (equipment and water costs are likely overhead).

- At the end of the period, the firm determines ending WIP percent completion and determines units completed.

- The equivalent production for each department is determined, which is later used to calculate the cost per unit of each job order by apportioning their total costs on basis of equivalent units.

In this illustration, Navarro is assumed to use the weighted-average costing method (other approaches such as FIFO could be used). This simplifies the process because the beginning inventory and current period production can be combined or “averaged” together. The following example is used to demonstrate how the equivalent units FIFO method is used to allocate production costs between completed and partially completed units. Under the FIFO method, the firm keeps beginning inventory costs attached to beginning inventory units. Those costs represent work done on equivalent units from last period. FIFO doesn’t intermingle work from last period with this period’s costs and this period’s rates.

Equivalent Units FIFO method

For the weighted average method, applying costs is relatively simple. You apply costs by multiplying the rates for direct materials, conversion costs, and transferred-in cost by (1) ending WIP equivalent units and (2) completed units. We must first FINISH beginning work in process, add units started and completed and units remaining in ending work in process. Beginning work in process is fully complete for materials (or 100% complete) and 60% complete for conversion so to complete these units we will need NO (or 0%) materials and 40% of conversion (100% – 60%). Units started and completed are always 100% complete for materials, labor and overhead!

Direct material is added in stages, such as the beginning, middle, or end of the process, while conversion costs are expensed evenly over the process. Often there is a different percentage of completion for materials than there is for labor. This leads to the very-important term total equivalent units (which I will sometimes abbreviate as TEU).

For the weighted average method, you add beginning balances to current period costs. At the end of the period, the firm determines ending WIP percent completion and determines units completed. Then the firm engages the following cycle to determine where the costs go.